View Procedure

| Procedure Name | Customs clearance procedure for importing goods for Duty Free shops |

|---|

| Description |

Required Documents

|

No.

|

Type of information

|

Note |

|

1

|

Foreign Trade Agreement or Price Invoice |

Documents necessary for declaration

|

| 2 |

Transportation documents.

|

| 3 |

Certificate of origin |

| 4 |

Permits and licenses required for goods subject to non-tariff restrictions

|

| 5 |

Conclusion issued by a specialized inspection agency on goods specifically specified in the legislation

|

| 6 |

Information on the goods such as the name, mark, purpose and classification code of the goods |

Process Steps

|

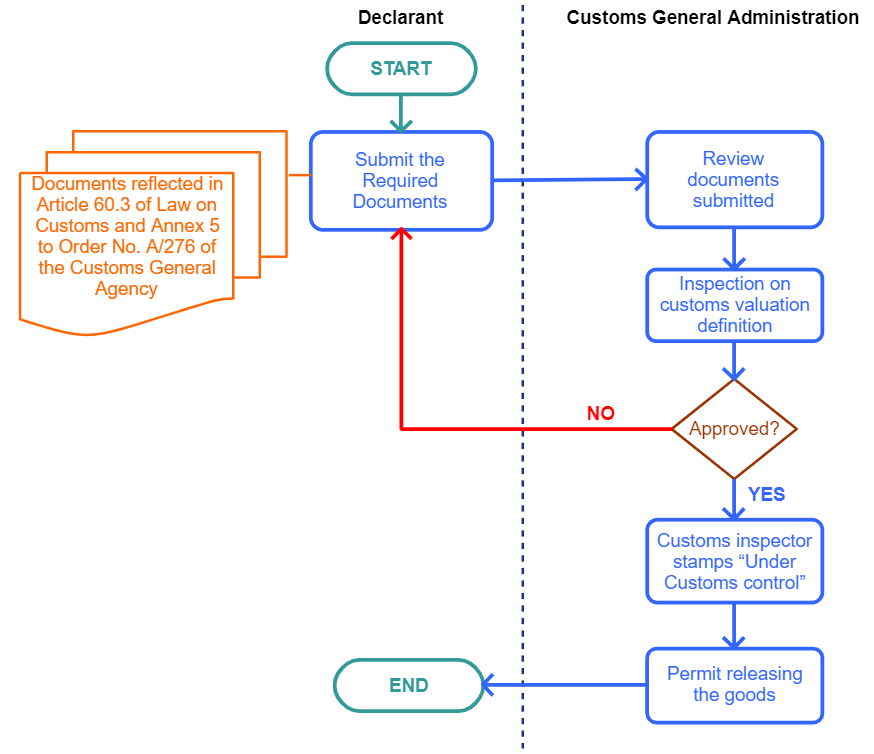

Step1

|

The declarant submits all necessary documents to Customs of Mongolia via e-mail, fax or through the customs information network

|

|

Step2

|

The State Customs Inspector in charge of control and inspection shall receive the information submitted through the Customs automated system,he shall verify the information recieved.

If necessary, customs may asks for more related documents or Information

|

| Step3 |

The customs declaration shall become effective upon the senior state customs inspector in charge of supervision and inspection performs the “Approve” action.

If a declarant submits a request, the Customs declaration shall be printed and the State Customs Inspector shall affix the “Under Customs Control” mark to the document, the State Customs Inspector shall and confirm it with a personal identification number.

|

| Step4 |

Levying customs duties, other taxes and fees

The Customs shall decide the Customs valuation method and whether a Customs value determined by a declarant is true, accurate and objective.

Where the documents supplied by declarant are not sufficient for verification of Customs value and decision-making, the Customs may require additional documents and information.

|

| Step5 |

Releasing goods and granting permission to import the goods across the customs border to a Customs bonded warehouse, Customs bonded construction site or Customs Guaranteed Exhibition Center |

|

NOTE

1. Customs and other taxes

1.1. Article 8 of the Law on Customs Tariffs and Customs Taxes

- The Customs may, on the basis of objective data, choose to determine Customs value by a method other than that applied by a declarant where;

- The documents used for determination of Customs value occur to be not valid, entries therein show discrepancy or are not complete or figures therein are insufficient; or

- A declarant fails to prove the truth and accuracy of Customs value and the Customs considers the Customs value determined by the declarant as groundless.

- In case of above the Customs and other taxes shall be assessed on the basis of a value determined by Customs using other method and charged to the declarant.

- In case where the Customs determined the Customs value, a declarant may get an exlanation in writing upon a written request to Customs.

- A declarant may, in contrary, refuse a value determined by Customs in case where he proved his declared value by presenting additional evidences within 45 days after the Customs declaration is validated.

- A declarant may, if he declines a value determined by Customs, appeal in accordance with the Customs law.

- A declarant is responsible for bearing any expenses incurred in the course of verification of Customs value.

- Where a Customs procedure is changed the value determined in the declaration by which the goods placed under the previous Customs procedure upon their crossing the national border shall not be changed.

|

|

|---|

| Category | Import |

|---|

The following form/s are used in this procedure

This procedure applies to the following measures